February Commentary

GLOBAL MARKETS

Global stock markets advanced despite a highly volatile month, driven by concerns over corporate earnings, intensifying AI competition, and potential tariff impacts.

US MARKETS

Mixed performance on strong earnings but AI uncertainty

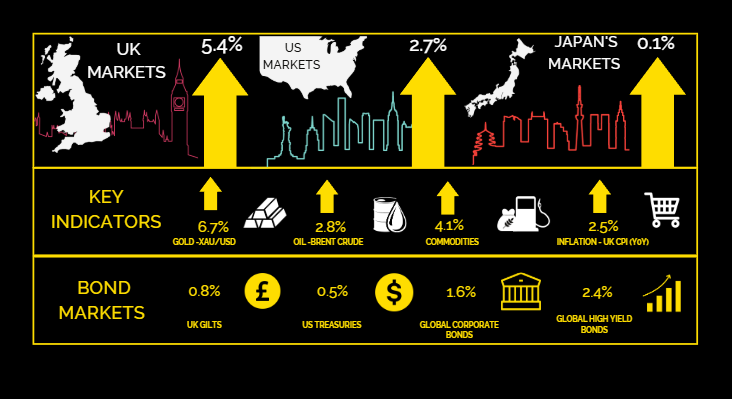

US equities advanced, driven by strong earnings from Meta and Apple. The US economy grew 2.3% in Q4, while the Fed held rates steady as the core Personal Consumption Expenditure (PCE) remained above 2%. The Nasdaq experienced significant volatility, as technology stocks sold off before recovering to end the month in positive territory. Competitive concerns over Chinese AI developer DeepSeek triggered a 17% one day drop in NVIDIA shares. Meanwhile, market sentiment was further weighed down by the US administration’s global tariff plans.

Up 2.7% (US 500)

UK MARKETS

Reached record highs on a weaker pound

UK equities advanced, reaching a record closing level, supported by a weaker pound, which boosted the FTSE100 by benefiting multinational firms with overseas revenues. The more defensive FTSE250 lagged noticeably by comparison. A rotation into defensive stocks provided further support as investors sought safe havens amid technology market volatility. Gains were also driven by strong corporate earnings, notably Shell’s announcement of a 4% dividend increase. However, signs of domestic economic weakness persisted, with two investment banks downgrading UK GDP forecasts for 2025. The government introduced a number of growth initiatives, including a controversial plan for a new Heathrow runway.

Up 5.4% (UK All Share)

EUROPEAN MARKETS

Strong on corporate earnings

European equity markets advanced, with the Stoxx Europe 600 gaining over 6%, driven by strong corporate earnings in technology, financials, and industrials. Easing concerns over US tariffs supported sentiment, though new tariff announcements later in the month introduced volatility. The ECB delivered its fifth rate cut in eight months, with President Lagarde signalling further easing. Euro-area GDP was flat in Q4 2024, with Germany contracting 0.2%, while Spain grew 0.8%. Inflation varied, with France at 1.8%, Germany at 2.8%, and Spain rising to 2.9%, reflecting mixed economic conditions.

Up 6.8% (Euro 600 Index ex UK)

JAPAN MARKETS

Pressured from technology sell-off

Japan’s stock markets posted marginal gains over the month, despite pressure from a sell-off in major technology stocks following the emergence of Chinese AI developer DeepSeek, a potential challenger to US dominance. Japanese chipmakers were particularly affected. Domestic equities also faced headwinds from the Bank of Japan’s (BoJ) hawkish stance, as it raised interest rates for the third time in a year and revised inflation forecasts upward. BoJ Deputy Governor Ryozo Himino reiterated the likelihood of further hikes if economic conditions align with forecasts. Meanwhile, Tokyo’s core CPI rose 2.5% year-on-year, reinforcing expectations for gradual policy tightening.

Up 0.1% (Japan Index)

Key Points

• The US dollar was mildly positive, strengthening against sterling, but declining against the yen and slightly against the euro. Tariff concerns continued to act as a tailwind.

• Sterling weakened as the UK economy struggled with sluggish growth and the strengthening of the US dollar.

• The Japanese yen strengthened against major currencies, supported by the Bank of Japan's (BoJ) third rate hike of the year. An upward revision in inflation forecasts, and the BoJ’s commitment to tightening policy, helped boost market confidence in the currency.

• The euro was mixed, strengthening against sterling but weakening against the US dollar and yen. It faces challenges from tariffs and the increased pace of ECB rate cuts.

Key Points

• UK gilts rose on the back of better inflation data, though the market remains sceptical about the government’s growth plan. The Bank of England is likely to cut rates in February, with expectations of two more cuts expected by year-end.

• US treasuries were marginally up, with the bond market relatively stable after weeks of uncertainty over Trump. There was no change to US interest rate expectations, with the market still pricing in two quarter-point cuts by the end of December.

• European sovereign bonds declined, as Christine Lagarde, ECB president, confirmed inflation is on track to hit 2% this year. Despite eurozone challenges, the ECB remains hawkish to align with the Fed and manage exchange rate pressures, while monitoring tariff uncertainties. The market anticipates three rate cuts by year-end.

• Investment-grade credit continued to perform well as spreads tightened further. The strongest returns came from high-yield and subordinated debt, which have performed very well in this 'risk-on' environment.

• Emerging market debt rose as uncertainty surrounding US President Trump's policy actions led to a risk-off sentiment across emerging markets.